The IRS has issued guidance providing relief from failure to make employment tax deposits for employers that are entitled to the refundable tax credits provided under two laws passed in response to the coronavirus (COVID-19) pandemic.

The two laws are the Families First Coronavirus Response Act, which was signed on March 18, 2020, and the Coronavirus Aid, Relief, and Economic Security Act (CARES) Act, which was signed on March 27, 2020.

The tax code imposes a penalty for any failure to deposit amounts as required on the date prescribed, unless such failure is due to reasonable cause rather than willful neglect.

An employer’s failure to deposit certain federal employment taxes, including deposits of withheld income taxes and taxes under the Federal Insurance Contributions Act (FICA) is generally subject to a penalty.

Employers paying qualified sick leave wages and qualified family leave wages required by the Families First Act, as well as qualified health plan expenses allocable to qualified leave wages, are eligible for refundable tax credits under the Families First Act.

Specifically, provisions of the Families First Act provide a refundable tax credit against an employer’s share of the Social Security portion of FICA tax for each calendar quarter, in an amount equal to 100% of qualified leave wages paid by the employer (plus qualified health plan expenses with respect to that calendar quarter).

Additionally, under the CARES Act, certain employers are also allowed a refundable tax credit under the CARES Act of up to 50% of the qualified wages, including allocable qualified health expenses if they are experiencing:

This credit is limited to $10,000 per employee over all calendar quarters combined.

An employer paying qualified leave wages or qualified retention wages can seek an advance payment of the related tax credits by filing Form 7200, Advance Payment of Employer Credits Due to COVID-19.

The Families First Act and the CARES Act waive the penalty for failure to deposit the employer share of Social Security tax in anticipation of the allowance of the refundable tax credits allowed under the two laws.

IRS Notice 2020-22 provides that an employer won’t be subject to a penalty for failing to deposit employment taxes related to qualified leave wages or qualified retention wages in a calendar quarter if certain requirements are met.

Contact David Mills, CPA, LLC for more information about whether you can take advantage of this relief.

During the COVID-19 health emergency, will your business receive a PPP payment?

The funds from the PPP (paycheck protection program) will hopefully be released soon. The best feature is that some or all of the loan can be forgiven.

However, please be aware, your banker will require strict documentation to have the loan forgiven.

While each bank may have slightly different paperwork requirements, we recommend the following:

If you need assistance with QuickBooks to implement the required record keeping please contact the staff at David Mills, CPA, LLC, for an appointment.

The IRS launched a new website to help those who don’t normally file a tax return register for the COVID-19 stimulus payments.

If you or a person you know doesn’t normally file a tax return, visit the newly established IRS Economic Impact Payments page.

This allows you to enter your banking information for direct deposit and register for the payment.

For more information about how the staff at David Mills, CPA, LLC can assist clients, contact us today.

The recently enacted Coronavirus Aid, Relief, and Economic Security (CARES) Act provides a refundable payroll tax credit for 50% of wages paid by eligible employers to certain employees during the COVID-19 pandemic.

The employee retention credit is available to employers, including nonprofit organizations, with operations that have been fully or partially suspended as a result of a government order limiting commerce, travel or group meetings.

The credit is also provided to employers who have experienced a greater than 50% reduction in quarterly receipts, measured on a year-over-year basis.

The credit is 50% of qualifying wages paid up to $10,000 in total. So the maximum credit for an eligible employer for qualified wages paid to any employee is $5,000. Wages paid after March 12, 2020, and before Jan. 1, 2021, are eligible for the credit. Therefore, an employer may be able to claim it for qualified wages paid as early as March 13, 2020. Wages aren’t limited to cash payments, but also include part of the cost of employer-provided health care.

The operation of a business is partially suspended if a government authority imposes restrictions by limiting commerce, travel or group meetings due to COVID-19 so that the business still continues but operates below its normal capacity.

Example: A state governor issues an executive order closing all restaurants and similar establishments to reduce the spread of COVID-19. However, the order allows establishments to provide food or beverages through carry-out, drive-through or delivery.

This results in a partial suspension of businesses that provided sit-down service or other on-site eating facilities for customers prior to the executive order.

No. The CARES Act doesn’t require employers to pay qualified wages.

No. Government employers aren’t eligible for the employee retention credit. Self-employed individuals also aren’t eligible for the credit for self-employment services or earnings.

Yes, but not for the same wages. The amount of qualified wages for which an employer can claim the employee retention credit doesn’t include the amount of qualified sick and family leave wages for which the employer received tax credits under the FFCRA.

No. An employer can’t receive the employee retention credit if it receives a Small Business Interruption Loan under the Paycheck Protection Program, which is authorized under the CARES Act. So an employer that receives a Paycheck Protection loan shouldn’t claim the employee retention credit.

For small businesses, the most attractive program built into the CARES Act (the federal coronavirus relief package) is the Payroll Protection Program (PPP).

The Payroll Protection Program is funded to the tune of $349 billion through the Small Business Administration (SBA).

However, the program differs in significant ways from the currently available Economic Injury Disaster Program.

First, businesses will apply through individual banks, not the SBA itself.

Second, while technically a loan program, a portion — and potentially all — of the loan can be forgiven, making it act more like a grant.

Eligibility – For-profit businesses with fewer than 500 employees (including hotels and food service businesses that have fewer than 500 employees per location); 501(c)(3) nonprofit organizations; veterans organizations; eligible self-employed individuals; independent contractors; sole proprietorships

Loan amount – The maximum loan size is equivalent to 250% of the employer’s average monthly payroll costs, not to exceed $10 million. Payroll costs are defined broadly to include wages, salaries, retirement contributions, healthcare benefits, covered leave, and other expenses. Put another way, the size of the loan is equal to the cost of payroll for about 10 weeks.

Loan terms – Up to 10 years at 4% with the ability to defer principal and interest payment for between 6 and 12 months. There are no fees, no requirement to secure the debt with collateral, no requirement of a personal guarantee, and no penalty for early payoff.

Loan forgiveness – A portion of the loan (up to 100%) will be forgiven in an amount equal to how much the business actually paid for payroll costs, salaries, benefits, rent, utilities and mortgage interest during the eight weeks following the loan’s disbursement. If employees are laid off or their salaries are reduced there could be a reduction in the amount forgiven. Borrowers will need to apply through their lender for this forgiveness and provide documentation for all costs. Banks will have 60 days to make the determination.

This information provided by the Greater Peoria Economic Development Council.

It’s very important that you contact your banker directly to apply for this program.

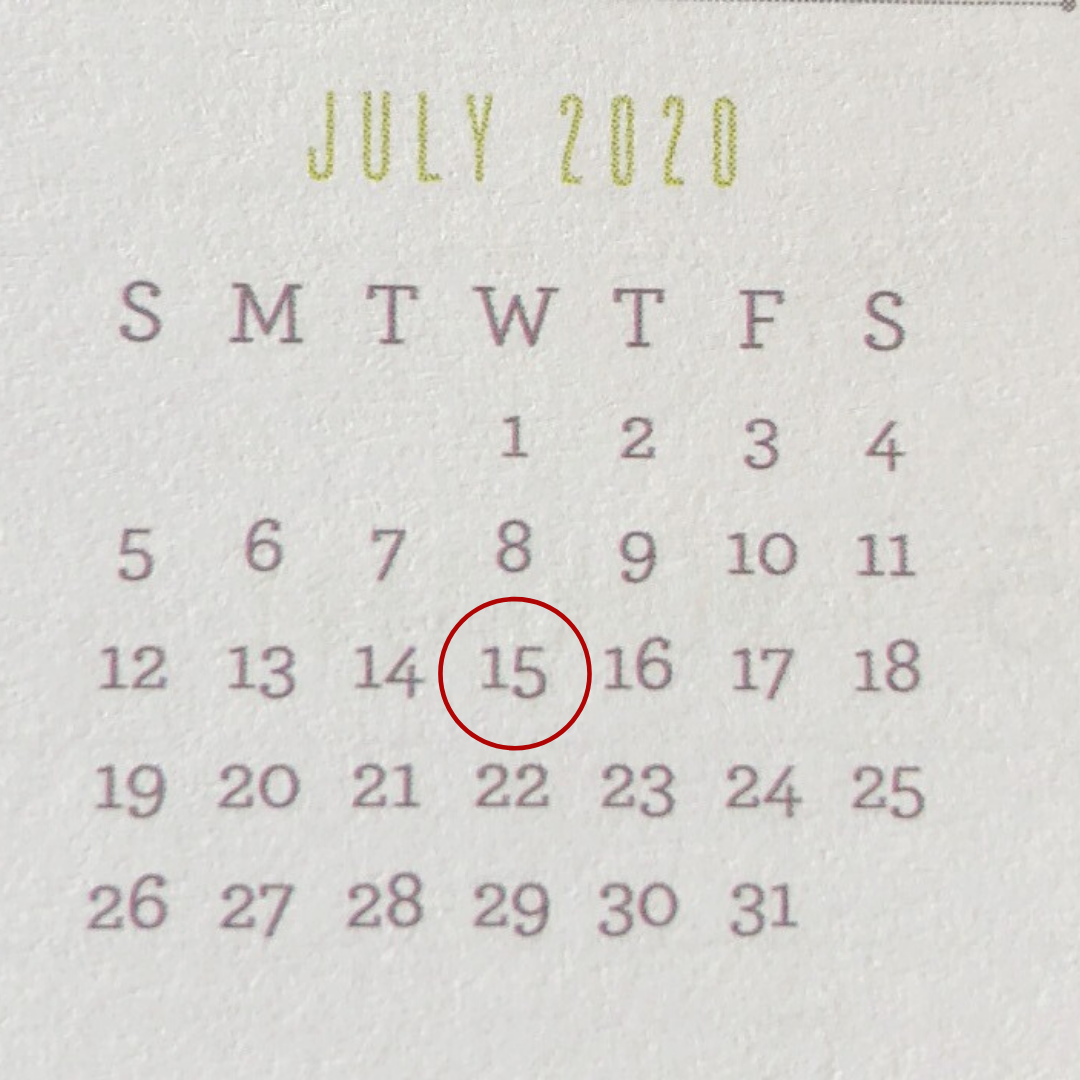

As a result of the COVID-19 virus and stay-at-home orders across the nation, the federal tax filing date has been extended to July 15, 2020. The State of Illinois also extended its deadline to July 15.

For more information, contact David Mills, CPA, LLC.

With the events of the last few days (closing of schools and extending the stay-at-home order until April 30th) it’s clear the COVID-19 virus threat is greater than expected.

To protect you and our staff at David Mills CPA, LLC, effective April 2, 2020, we will no longer be meeting with clients until the stay-at-home order is lifted. Our doors will be locked, and reception areas will be closed to walk-ins.

Our staff is still providing all the services we normally do. We continue to prepare tax returns, bookkeeping and payroll services.

For payroll clients: We will contact you about payroll delivery. This is a good time to consider direct deposit for employees. We’ll keep you updated on events as they happen.

Thank you for your understanding and patience during these unprecedented times.

If you’re self-employed and work out of an office in your home, you may be entitled to home business deductions. However, you must satisfy strict rules.

If you qualify, you can deduct the “direct expenses” of the home office. This includes the costs of painting or repairing the home office and depreciation deductions for furniture and fixtures used there.

You can also deduct the “indirect” expenses of maintaining the office. This includes the allocable share of utility costs, depreciation, and insurance for your home, as well as the allocable share of mortgage interest, real estate taxes and casualty losses.

In addition, if your home office is your “principal place of business,” the costs of traveling between your home office and other work locations are deductible transportation expenses, rather than nondeductible commuting costs.

And, generally, you can deduct the cost (reduced by the percentage of non-business use) of computers and related equipment that you use in your home office, in the year that they’re placed into service.

You can deduct your expenses if you meet any of these three tests:

You’re entitled to deductions if you use your home office, exclusively and regularly, as your principal place of business. Your home office is your principal place of business if it satisfies one of two tests.

You satisfy the “management or administrative activities test” if you use your home office for administrative or management activities of your business, and you meet certain other requirements.

You meet the “relative importance test” if your home office is the most important place where you conduct business, compared with all the other locations where you conduct that business.

You’re entitled to home office deductions if you use your home office, exclusively and regularly, to meet or deal with patients, clients, or customers.

The patients, clients or customers must physically come to the office.

You’re entitled to home office deductions for a home office, used exclusively and regularly for business, that’s located in a separate unattached structure on the same property as your home. For example, this could be in an unattached garage, artist’s studio or workshop.

You may also be able to deduct the expenses of certain storage space for storing inventory or product samples. If you’re in the business of selling products at retail or wholesale, and if your home is your sole fixed business location, you can deduct home expenses allocable to space that you use to store inventory or product samples.

The amount of your home office deductions is subject to limitations based on the income attributable to your use of the office, your residence-based deductions that aren’t dependent on use of your home for business (such as mortgage interest and real estate taxes), and your business deductions that aren’t attributable to your use of the home office.

But any home office expenses that can’t be deducted because of these limitations can be carried over and deducted in later years.

Be aware that if you sell — at a profit — a home that contains (or contained) a home office, there may be tax implications. We can explain them to you. Pin down the best tax treatment Proper planning can be the key to claiming the maximum deduction for your home office expenses.

For business structure and tax advice, contact the experts at David Mills, CPA, LLC. Our offices are located in Morton and East Peoria.

As a small-business owner, it always helps to have expert advice at your fingertips. A QuickBooks ProAdvisor offers that expertise.

For small and medium-sized businesses, QuickBooks is one of the most popular accounting software programs available.

Using QuickBooks, businesses can manage and pay bills, keep track of accounts payable and receivable, oversee financial reporting, organize payroll functions and track employee time.

Relying on a QuickBooks ProAdvisor ensures your business gets the most out of the accounting software.

QuickBook ProAdvisors must complete comprehensive training and pass a certification exam to earn the ProAdvisor title.

The certification ensures all ProAdvisors are experts in the latest QuickBook tools and can help customize QuickBook software to fit your business needs.

At David Mills, CPA, LLC, we have QuickBooks ProAdvisors on staff who are able to train and assist you with all your QuickBooks needs.

We provide one-on-one or small group QuickBooks training sessions, and our on-staff experts can meet in person. Our training is geared toward your business.

Our ProAdvisors will help design and set up the chart of accounts as well as set up payroll, receivables, payables, inventory and other features needed by your business.

To learn more about how a QuickBooks ProAdvisor from David Mills, CPA, LLC can benefit your business, contact us today. We have offices in both Morton and East Peoria.

The federal government recently extended the Work Opportunity Tax Credit through 2020. Business owners may be eligible for tax credits if they hire individuals from one or more targeted groups.

The Work Opportunity Tax Credit (WOTC) was set to expire on Dec. 31, 2019, but a new law passed late last year extends it through Dec. 31, 2020.

Generally, an employer is eligible for the credit for qualified wages paid to qualified members of these targeted groups:

For each employee, there’s a minimum requirement that the employee has completed at least 120 hours of service for the employer.

The credit isn’t available for certain employees who are related to the employer or work more than 50% of the time outside of a trade or business of the employer (for example, a maid working in the employer’s home).

Additionally, the credit generally isn’t available for employees who’ve previously worked for the employer.

There are different rules and credit amounts for certain employees.

The maximum credit available for the first-year wages is $2,400 for each employee, $4,000 for long-term family assistance recipients, and $4,800, $5,600 or $9,600 for certain veterans.

Additionally, for long-term family assistance recipients, there’s a 50% credit for up to $10,000 of second-year wages, resulting in a total maximum credit, over two years, of $9,000.

For summer youth employees, the wages must be paid for services performed during any 90-day period between May 1 and September 15.

The maximum WOTC credit available for summer youth employees is $1,200 per employee.

No deduction is allowed for the portion of wages equal to the amount of the WOTC determined for the tax year.

Other employment-related credits are generally reduced with respect to an employee for whom a WOTC is allowed.

The credit is subject to the overall limits on the amount of business credits that can be taken in any tax year, but a 1-year carryback and 20-year carryforward of unused business credits is allowed.

Because of these rules, there may be circumstances when the employer might elect not to have the WOTC apply. There are some additional rules that, in limited circumstances, prohibit the credit or require an allocation of it.

For more information, or to see if the WOTC would apply to your business, contact the tax professionals at David Mills CPA, LLC. Our offices are located in Morton and East Peoria.