At the moment, tax rates are at historic lows. We have record deficits and are looking to add more. Where do you think tax rates will be at in 1 year? 3 years? 5 years or more? Here are a few things to consider when thinking about taxes in 2020.

While everyone’s situation is different, we believe this is a serious consideration in tax planning for many individuals.

Most IRA fund balances are at a low point and many taxpayers may see lower income in 2020. This may be a good time to convert some or all your funds to a Roth IRA.

You can manage the tax brackets. For example, an estimate of income can be prepared to find out how much more income you can have to stay in the same tax bracket. This way you can effectively manage your tax burden.

If your modified adjusted gross income in 2020 for married filing jointly is $196,000 or less you can contribute directly to a Roth IRA. Income at $206,000 cannot make a Roth contribution.

You can contribute to a traditional IRA. You can then convert to a Roth IRA. There are other limitations so be sure to discuss this with your financial adviser or make an appointment with us to discuss how this works and if a conversion will help you in retirement.

The IRS has a $300 cash (not non-cash such as a Goodwill donation) charitable deduction for 2020 which can be used whether you itemize or not.

If you have not begun taking required minimum distributions (RMD’s) in 2020 you can wait until age 72 to start. The previous rules were at age 70 ½. Note that if you have already started your RMD’s you cannot skip them until age 72-you are bound by the previous rules.

There are other considerations for this so it is best to consult your financial adviser.

If you have questions, please talk to the experts at David Mills, CPA, LLC, today. We would be happy to help! Contact us today.

As a result of the coronavirus (COVID-19) crisis, your business may be using independent contractors to keep costs low. But you should be careful that these workers are properly classified for federal tax purposes. If the IRS reclassifies them as employees, it can be an expensive mistake.

The question of whether a worker is an independent contractor or an employee for federal income and employment tax purposes is a complex one.

If a worker is an employee, your company must withhold federal income and payroll taxes, pay the employer’s share of FICA taxes on the wages, plus FUTA tax.

Often, a business must also provide the worker with the fringe benefits that it makes available to other employees. And there may be state tax obligations as well. These obligations don’t apply if a worker is an independent contractor.

In that case, the business simply sends the contractor a Form 1099-MISC for the year showing the amount paid (if the amount is $600 or more).

Who is an “employee?” Unfortunately, there’s no uniform definition of the term. The IRS and courts have generally ruled that individuals are employees if the organization they work for has the right to control and direct them in the jobs they’re performing.

Otherwise, the individuals are generally independent contractors. But other factors are also taken into account. Some employers that have misclassified workers as independent contractors may get some relief from employment tax liabilities under Section 530.

In general, this protection applies only if an employer:

Note: Section 530 doesn’t apply to certain types of technical services workers. And some categories of individuals are subject to special rules because of their occupations or identities.

Under certain circumstances, you may want to ask the IRS (on Form SS-8) to rule on whether a worker is an independent contractor or employee.

However, be aware that the IRS has a history of classifying workers as employees rather than independent contractors.

Businesses should consult with the staff at David Mills, CPA, LLC before filing Form SS-8 because it may alert the IRS that your business has worker classification issues — and inadvertently trigger an employment tax audit.

It may be better to properly treat a worker as an independent contractor so that the relationship complies with the tax rules. Be aware that workers who want an official determination of their status can also file Form SS-8.

Disgruntled independent contractors may do so because they feel entitled to employee benefits and want to eliminate self-employment tax liabilities. If a worker files Form SS-8, the IRS will send a letter to the business. It identifies the worker and includes a blank Form SS-8.

The business is asked to complete and return the form to the IRS, which will render a classification decision.

Contact the small business experts at David Mills, CPA, LLC if you’d like to discuss how these complex rules apply to your business.

The Paycheck Protection Program (PPP) established by the U.S. Government as part of the CARES Act is designed to help businesses during the COVID-19 pandemic.

For businesses who are part of the Paycheck Protection Program, there are a few tips and guidelines to know and understand:

For more information, contact the experts at David Mills, CPA, LLC.

To help you wade through all the information about the COVID-19 stimulus payment, also known as the Economic Impact Payment, we’re offering tips to a few key things you should know:

For more information, contact the tax professionals at David Mills, CPA, LLC.

The IRS has issued guidance providing relief from failure to make employment tax deposits for employers that are entitled to the refundable tax credits provided under two laws passed in response to the coronavirus (COVID-19) pandemic.

The two laws are the Families First Coronavirus Response Act, which was signed on March 18, 2020, and the Coronavirus Aid, Relief, and Economic Security Act (CARES) Act, which was signed on March 27, 2020.

The tax code imposes a penalty for any failure to deposit amounts as required on the date prescribed, unless such failure is due to reasonable cause rather than willful neglect.

An employer’s failure to deposit certain federal employment taxes, including deposits of withheld income taxes and taxes under the Federal Insurance Contributions Act (FICA) is generally subject to a penalty.

Employers paying qualified sick leave wages and qualified family leave wages required by the Families First Act, as well as qualified health plan expenses allocable to qualified leave wages, are eligible for refundable tax credits under the Families First Act.

Specifically, provisions of the Families First Act provide a refundable tax credit against an employer’s share of the Social Security portion of FICA tax for each calendar quarter, in an amount equal to 100% of qualified leave wages paid by the employer (plus qualified health plan expenses with respect to that calendar quarter).

Additionally, under the CARES Act, certain employers are also allowed a refundable tax credit under the CARES Act of up to 50% of the qualified wages, including allocable qualified health expenses if they are experiencing:

This credit is limited to $10,000 per employee over all calendar quarters combined.

An employer paying qualified leave wages or qualified retention wages can seek an advance payment of the related tax credits by filing Form 7200, Advance Payment of Employer Credits Due to COVID-19.

The Families First Act and the CARES Act waive the penalty for failure to deposit the employer share of Social Security tax in anticipation of the allowance of the refundable tax credits allowed under the two laws.

IRS Notice 2020-22 provides that an employer won’t be subject to a penalty for failing to deposit employment taxes related to qualified leave wages or qualified retention wages in a calendar quarter if certain requirements are met.

Contact David Mills, CPA, LLC for more information about whether you can take advantage of this relief.

During the COVID-19 health emergency, will your business receive a PPP payment?

The funds from the PPP (paycheck protection program) will hopefully be released soon. The best feature is that some or all of the loan can be forgiven.

However, please be aware, your banker will require strict documentation to have the loan forgiven.

While each bank may have slightly different paperwork requirements, we recommend the following:

If you need assistance with QuickBooks to implement the required record keeping please contact the staff at David Mills, CPA, LLC, for an appointment.

The IRS launched a new website to help those who don’t normally file a tax return register for the COVID-19 stimulus payments.

If you or a person you know doesn’t normally file a tax return, visit the newly established IRS Economic Impact Payments page.

This allows you to enter your banking information for direct deposit and register for the payment.

For more information about how the staff at David Mills, CPA, LLC can assist clients, contact us today.

The recently enacted Coronavirus Aid, Relief, and Economic Security (CARES) Act provides a refundable payroll tax credit for 50% of wages paid by eligible employers to certain employees during the COVID-19 pandemic.

The employee retention credit is available to employers, including nonprofit organizations, with operations that have been fully or partially suspended as a result of a government order limiting commerce, travel or group meetings.

The credit is also provided to employers who have experienced a greater than 50% reduction in quarterly receipts, measured on a year-over-year basis.

The credit is 50% of qualifying wages paid up to $10,000 in total. So the maximum credit for an eligible employer for qualified wages paid to any employee is $5,000. Wages paid after March 12, 2020, and before Jan. 1, 2021, are eligible for the credit. Therefore, an employer may be able to claim it for qualified wages paid as early as March 13, 2020. Wages aren’t limited to cash payments, but also include part of the cost of employer-provided health care.

The operation of a business is partially suspended if a government authority imposes restrictions by limiting commerce, travel or group meetings due to COVID-19 so that the business still continues but operates below its normal capacity.

Example: A state governor issues an executive order closing all restaurants and similar establishments to reduce the spread of COVID-19. However, the order allows establishments to provide food or beverages through carry-out, drive-through or delivery.

This results in a partial suspension of businesses that provided sit-down service or other on-site eating facilities for customers prior to the executive order.

No. The CARES Act doesn’t require employers to pay qualified wages.

No. Government employers aren’t eligible for the employee retention credit. Self-employed individuals also aren’t eligible for the credit for self-employment services or earnings.

Yes, but not for the same wages. The amount of qualified wages for which an employer can claim the employee retention credit doesn’t include the amount of qualified sick and family leave wages for which the employer received tax credits under the FFCRA.

No. An employer can’t receive the employee retention credit if it receives a Small Business Interruption Loan under the Paycheck Protection Program, which is authorized under the CARES Act. So an employer that receives a Paycheck Protection loan shouldn’t claim the employee retention credit.

For small businesses, the most attractive program built into the CARES Act (the federal coronavirus relief package) is the Payroll Protection Program (PPP).

The Payroll Protection Program is funded to the tune of $349 billion through the Small Business Administration (SBA).

However, the program differs in significant ways from the currently available Economic Injury Disaster Program.

First, businesses will apply through individual banks, not the SBA itself.

Second, while technically a loan program, a portion — and potentially all — of the loan can be forgiven, making it act more like a grant.

Eligibility – For-profit businesses with fewer than 500 employees (including hotels and food service businesses that have fewer than 500 employees per location); 501(c)(3) nonprofit organizations; veterans organizations; eligible self-employed individuals; independent contractors; sole proprietorships

Loan amount – The maximum loan size is equivalent to 250% of the employer’s average monthly payroll costs, not to exceed $10 million. Payroll costs are defined broadly to include wages, salaries, retirement contributions, healthcare benefits, covered leave, and other expenses. Put another way, the size of the loan is equal to the cost of payroll for about 10 weeks.

Loan terms – Up to 10 years at 4% with the ability to defer principal and interest payment for between 6 and 12 months. There are no fees, no requirement to secure the debt with collateral, no requirement of a personal guarantee, and no penalty for early payoff.

Loan forgiveness – A portion of the loan (up to 100%) will be forgiven in an amount equal to how much the business actually paid for payroll costs, salaries, benefits, rent, utilities and mortgage interest during the eight weeks following the loan’s disbursement. If employees are laid off or their salaries are reduced there could be a reduction in the amount forgiven. Borrowers will need to apply through their lender for this forgiveness and provide documentation for all costs. Banks will have 60 days to make the determination.

This information provided by the Greater Peoria Economic Development Council.

It’s very important that you contact your banker directly to apply for this program.

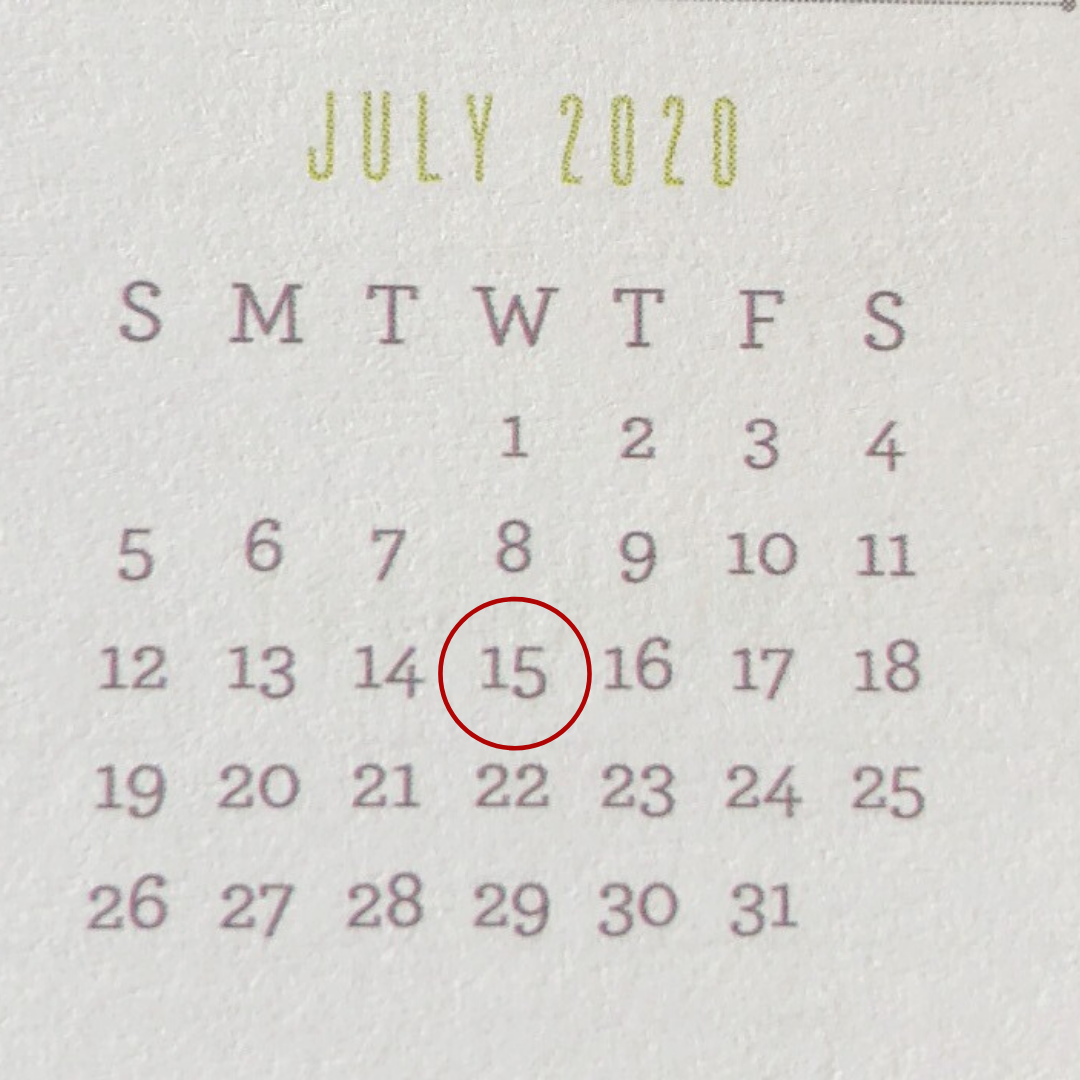

As a result of the COVID-19 virus and stay-at-home orders across the nation, the federal tax filing date has been extended to July 15, 2020. The State of Illinois also extended its deadline to July 15.

For more information, contact David Mills, CPA, LLC.